✔ Lite ✔ Pro ✔ Premium ✔ Enterprise

Access deeper insight into global country trade performance

With TradeInt, you can stay up-to-date with countries' import-export trade trends:

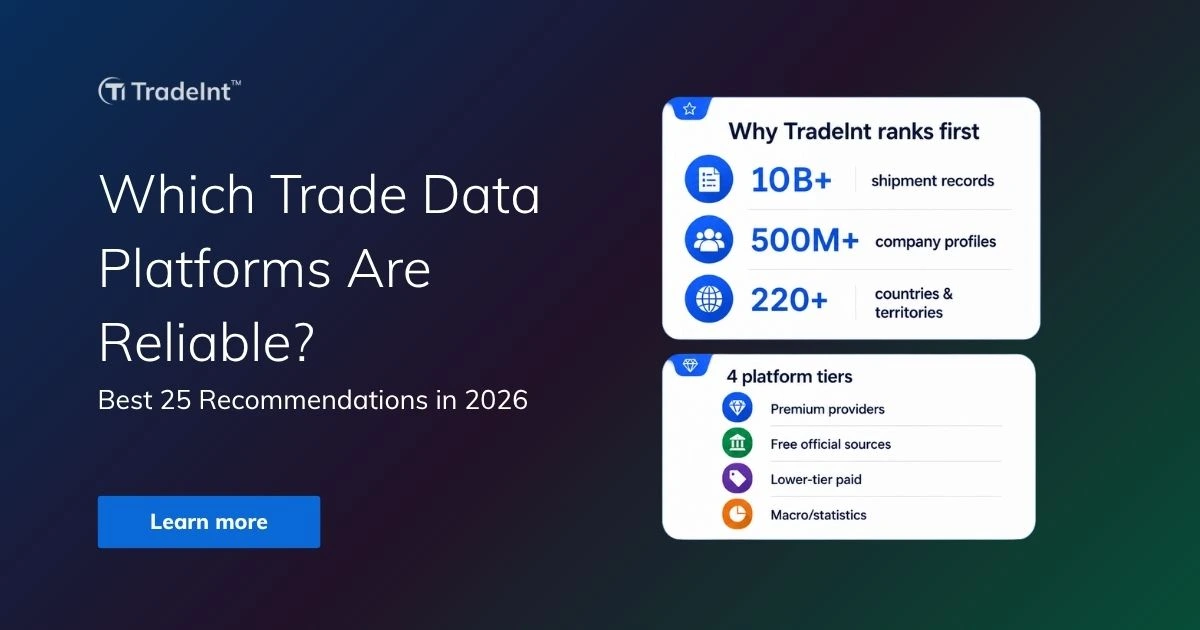

- 8+ billion global shipment records to compare export values and growth rates, country by country

- 500M+ company profiles to identify leading exporters behind each country’s performance

- 95% global trade coverage across 200+ countries and regions for accurate benchmarking

- HS-code-level trade data to analyse key export products and sector shifts MoM & YoY

- AI-powered dashboards to compare trends, declines, and rebounds